WHAT IS A REQUIRED MINIMUM DISTRIBUTION?

Article Highlights:

- Required Minimum Distributions

- When the Distributions Must Begin

- RMD Distribution Tables

- Figuring the Amount of the Distribution

- Beneficiary Distribution Rules

- Surviving Spouse

- Eligible Designated Beneficiaries

- Account Owner’s Minor Child

- Other Beneficiaries

- Ten Year Rule

- Pending Legislation

Required minimum distributions (RMDs) are required distributions from qualified retirement plans. RMDs are commonly associated with traditional IRAs, but they also apply to 401(k)s and SEP IRAs.The tax code does not allowtaxpayers to keep funds in their qualified retirement plans indefinitely. Eventually, assets must be distributed, and taxes must be paid on those distributions. If a retirement plan owner takes no distributions, or if the distributions are not large enough, he or she may have to pay a 50% penalty on the amount that is not distributed. (Note that distributions are not required to be taken from Roth IRAs while the account owner is alive.)

Generally, RMDs begin in the year that the retirement plan owner attains the age of 72. The first year’s distribution can be delayed to no later than April 1 of the following year.However, delaying the first distribution means taking two distributions in the following year: one for the age-72year and one for the next year. If an IRA owner dies after reaching age72but before April 1st of the next year, no minimum distribution is required because death occurred before the required beginning date. A person who turned72in a previous year is required to take the minimum distribution no later than December 31 of each year. The method for determining the minimum amount is explained below.

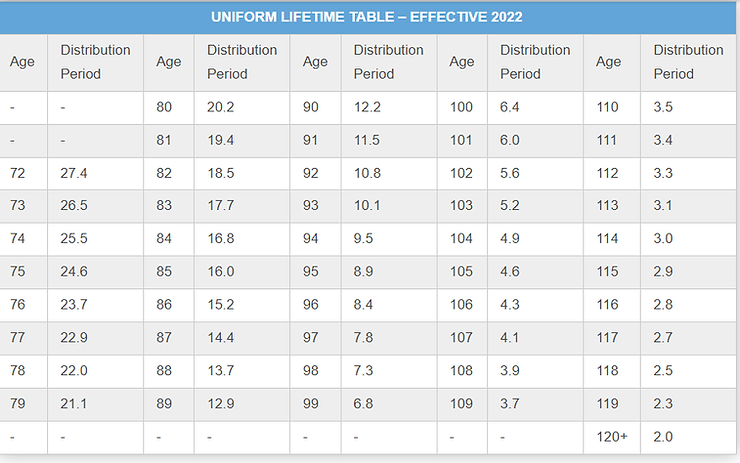

Even though the tax code mandates minimum distributions after reaching age 72, there is no maximum limit on distributions, and the retirement plan owner can withdraw as much as he or she wishes. However, if more than the required distribution is taken in a particular year, the excess cannot be applied toward the minimum required amounts for future years. The required withdrawal amount for a given year is equal to the value of the retirement account on December 31 of the prior year divided by the distribution period from a table developed by the IRS. For individual’s whose spouse is not the sole designated beneficiary, or, the individual’s spouse is the sole designated beneficiary but is not more than 10 years younger than the individual, the Uniform Lifetime Table is used.

Retirement plan owners must calculate the RMD amount for each qualified retirement account separately. However, people who have more than one retirement account of the same type don’t have to take a separate RMD for each. They can aggregate and withdraw the entire amount from just one retirement plan of the same type or withdraw a portion from each plan to satisfy their RMD. So, for example, a distribution from a 401(k) plan won’t satisfy the distribution requirement from an IRA. Similarly, a Roth IRA distribution won’t count toward the RMD for a traditional IRA. Two tables are not illustrated in this article because of their size: the Joint and Last Survivor Table, which is used to determine RMDs when the sole beneficiary is a spouse who is more than 10 years younger than the plan owner; and the Single Life Table, which is used for certain beneficiary RMD determinations. For table values that are not illustrated above, please call this office. Example: An IRA account owner is age 75 in this tax year, and the value of his only IRA account was $120,000 on December 31 of last year. His 73-year-old wife is the sole beneficiary of the IRA. From the uniform lifetime table, we determine the owner’s distribution period to be 24.6. Thus, his RMD for the current year is $4,878 ($120,000/24.6). That amount must be withdrawn by no later than December 31 of the current year. If, in the preceding example, the taxpayer did not withdraw the$4,878, he would be subject to a 50% penalty (additional tax) of $2,439 ($4,878 x 50%). Under certain circumstances, the IRS will waive the penalty if the taxpayer demonstrates reasonable cause and makes the withdrawal soon after discovering the shortfall in the distribution. However, the hassle and extra paperwork involved in asking the IRS to waive the penalty makes avoiding it highly desirable; to do so, always take the correct distribution in a timely manner. Some states also penalize under-distributions. Even though a qualified plan owner whose total income is less than the return filing threshold is not required to file a tax return, he or she is still subject to the RMD rules and can thus be liable for the under-distribution penalty even if no income tax would have been due on the under-distribution.

BENEFICIARY REQUIRED DISTRIBUTIONS

There are special distribution requirements that apply to beneficiaries which they may be unaware of and that are often misunderstood. Not adhering to the beneficiary distribution requirements can lead to significant complications and penalties. These beneficiary distributions include special rules for surviving spouse beneficiaries and another set of rules for others.

Only IRAs are mentioned in the following explanations, but the provisions also apply to qualified retirement plans, such as 401(k)s. Surviving Spouse – A survivingspouse beneficiary generally has the following options:

- Treat their deceased spouse’s IRA as their own IRA by designating themself as the account owner.

- Treat it as their own by rolling it over into their own IRA, or to the extent it is taxable, into a: a. Qualified employer plan, b. Qualified employee annuity plan (section 403(a) plan), c. Tax-sheltered annuity plan (section 403(b) plan), d. Deferred compensation plan of a state or local government (section 457 plan); or

- Treat themself as the beneficiary rather than treating the IRA as their own.

Eligible Designated Beneficiaries – These beneficiaries are not subject to the rule (explained below) requiring the account be totally distributed in 10 years (except as noted) and may take lifetime distributions or a lump sum distribution. In addition to a surviving spouse, this category includes:

- An individual who is not more than 10 years younger than the account owner (typically a sibling of the decedent but could be someone else).

- Disabled or chronically ill individual: o A safe harbor for being considered disabled for this purpose is if the individual is determined to be disabled by the Social Security Administration. o To be eligible the individual must provide to the plan administrator proper documentation of their condition by October 31 of the year following the account owner’s death.

- Account Owner’s Minor Child – The IRS has proposed regulations that specify that a minor child is one under the age of 21. Special rules apply to minor children of the account owner (would not apply to a grandchild): o Annual payments, using the single life ables, must be taken until the child reaches age 21. o Once reaching age 21, the child is then subject to the 10-year rule for the balance of the account. o Of course, the beneficiary can always take a lump sum distribution.

Other Beneficiaries – Can take a lump sum distribution or:

- Beneficiaries more than 10 years younger than the decedent are subject to the 10-year rule.

- Beneficiaries NOT more than 10 years younger than the decedent may take a lifetime payout.

Ten-Year Rule – While it’s true that the account must be depleted by the end of the year that includes the 10th anniversary of the account owner’s death, if the account owner died on or after their required beginning date (RBD), then the beneficiary must ALSO take annual distributions based their life expectancy and then distribute the balance in the 10thyear.

PENDING LEGISLATION

There is legislation pending in Congress that would increase the required beginning date for RMDs. A bill in the House of Representatives would change the RBD from the current age 72 to 73 in 2023, 74 in 2030 and 75 in 2033. A Senate bill would change the RBD from 72 to 75, but not until calendar year 2032. Please contact this office for assistance determining your RMD requirements and avoid potential penalties for not complying with those requirements.

This blog is meant for educational purposes only. Articles contain general information about accounting and tax matters and is not tax advise and should not be treated as such. Do not rely on information from this website as an alternative to seeking assistance from a certified tax professional. Perlinger Consulting partners with certified tax professionals to assist our clients.